Building a custom home in California means dealing with a financing process that works nothing like a standard mortgage. Construction loans in California are structured around the build timeline, not the final property value, and knowing how they work can save you from serious budget and timeline mistakes. This guide breaks down everything custom home builders and property investors need to know before breaking ground.

What Is a Construction Loan and How Does It Work?

A construction loan is short-term financing designed specifically to fund a home build from the ground up. Unlike a standard mortgage that covers a property with an existing value, construction loans in California are structured around the build timeline itself.

The key difference in how funds work:

- Staged disbursement: Money is released in phases called “draws,” each tied to a completed milestone like foundation, framing, or roofing.

- Lender inspections: Before each draw is released, the lender sends an inspector to verify the work is actually done.

- Interest-only payments: During construction, you only pay interest on the amount drawn so far, not the full loan balance.

Once construction wraps up and the Certificate of Occupancy is issued, the loan either converts to a permanent mortgage or is refinanced, depending on the structure you chose at the start.

What makes construction lending different from a regular home loan is that lenders evaluate two things at once: your financial profile as a borrower, and the viability of the project itself. The builder’s credentials, the architectural plans, the cost breakdown, and the projected finished value all factor into the approval decision.

Types of Construction Loans Available in California

California borrowers have several loan structures to choose from, and the right option depends on your project scope, financial profile, and how much flexibility you need during the build.

Construction-to-Permanent Loan (One-Time Close)

The most common choice for custom home builders. This single loan covers both the construction phase and the long-term mortgage, with one closing, one set of closing costs, and a locked interest rate from the start. When construction ends, it automatically converts to a standard mortgage.

Construction-Only Loan (Two-Close)

Covers the build phase only. Once construction is complete, you pay it off by taking out a separate mortgage. More flexibility, but two rounds of closing costs and no rate lock on the permanent loan.

Owner-Builder Loan

Designed for borrowers who want to act as their own general contractor. Lenders apply significantly stricter requirements here, typically requiring a contractor’s license or demonstrated project management experience.

Renovation and ADU Loans

Used for major remodels or adding an accessory dwelling unit. Loan amounts are based on the projected value of the property after completion, not its current value.

Here’s a quick comparison of the most common options:

| Loan Type | Closings | Best For |

| Construction-to-Permanent | 1 | Custom home builds, rate certainty |

| Construction-Only | 2 | Investors, flexible end financing |

| Owner-Builder | 1 or 2 | Licensed or experienced builders |

| Renovation / ADU | 1 | Remodels, additions, ADU projects |

One thing worth knowing for Bay Area projects specifically: construction costs in cities like Cupertino, San Jose, and Palo Alto often push total project values well above conforming loan limits, which means you’ll likely need a jumbo construction loan. Not every lender offers these, so confirming this upfront saves time.

The Step-by-Step Process: From Loan Approval to Move-In Day

Knowing what to expect at each stage helps you avoid delays and keeps the project moving on schedule.

1. Get Pre-Qualified

Before anything else, talk to a lender who specializes in construction loans in California. General mortgage lenders often lack the underwriting experience for ground-up builds. Pre-qualification gives you a realistic budget ceiling before you commit to land, plans, or a builder.

2. Choose Your Builder and Finalize Plans

Lenders require a licensed, insured contractor with a verifiable project history. At this stage you’ll also need complete architectural drawings, a detailed cost breakdown, and a construction timeline. Incomplete documentation is the most common reason for approval delays.

A strong Custom Home Design process that accounts for lender requirements from day one keeps your plans from needing costly revisions down the line.

3. Loan Application and Underwriting

The lender evaluates both your financial profile and the project itself. An independent appraiser estimates the completed home’s value based on your plans and local comparables. In high-value markets like Cupertino or Palo Alto, this appraisal directly determines your maximum loan amount.

4. Loan Closing and Construction Start

Once approved, you close on the loan and the builder can break ground. From this point, funds are released through the draw schedule you agreed on at closing.

5. Draw Inspections

At each construction milestone, the lender inspects the completed work before releasing the next draw. Staying on schedule here keeps cash flow predictable for your builder and avoids unnecessary project interruptions.

6. Final Inspection and Certificate of Occupancy

When construction is complete, the local building department conducts a final inspection. The Certificate of Occupancy officially marks the end of the construction phase.

7. Loan Conversion or Refinance

With a construction-to-permanent loan, the balance automatically converts to a standard mortgage. With a construction-only loan, you now apply for a separate mortgage to pay off the construction balance.

Construction Loan Requirements in California: What Lenders Look For

Getting approved for a construction loan in California is more involved than qualifying for a standard mortgage. Lenders are not just evaluating you as a borrower; they are also assessing whether the project itself is financially viable and likely to be completed on time. That means your credit profile, your finances, your builder, and your project plans all go through scrutiny before a single dollar is released.

Credit Score Requirements

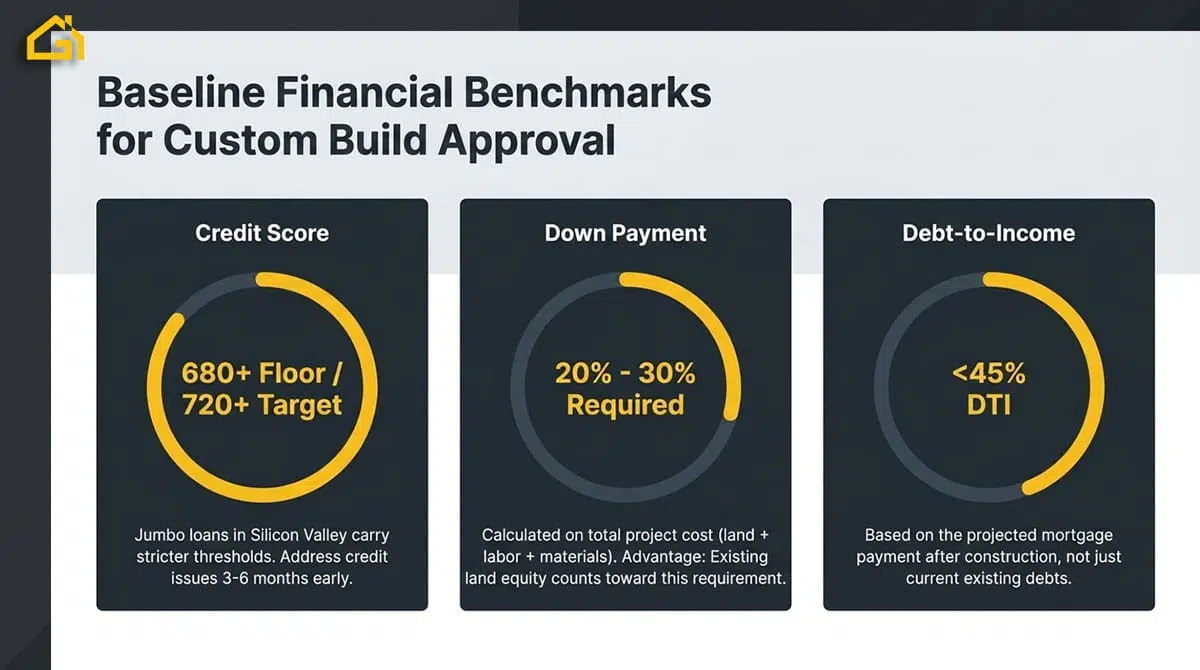

Most lenders require a minimum credit score of 680 for a construction loan in California, though many prefer 700 or higher, especially for jumbo loans in high-cost markets like the Bay Area. The higher your score, the better your chances of securing a competitive interest rate and favorable loan terms.

A few things worth knowing:

- 680 is typically the floor, not the target. Borrowers in the 720+ range tend to get smoother approvals and better pricing.

- Jumbo construction loans (common in cities like Cupertino, Palo Alto, and San Jose) often carry stricter credit requirements than conforming loan products.

- Recent credit events like late payments, collections, or high utilization can complicate approval even if your score technically meets the threshold.

Before applying, it is worth pulling your credit report and addressing any issues at least three to six months in advance. Lenders in this space have less flexibility than conventional mortgage lenders, and underwriting tends to be more conservative.

Down Payment

Construction loans in California typically require between 20% and 30% down, calculated on the total project cost including land, labor, and materials. If you already own the land, its appraised value can often count toward this requirement, which reduces the cash you need at closing.

Bay Area construction costs are among the highest in the country, and getting your numbers right before applying is what separates a smooth approval from a stalled one.

Debt-to-Income Ratio

Lenders generally look for a DTI at or below 45%, based on your projected mortgage payment after construction, not just your current debts. If your ratio is borderline, paying down existing obligations before applying is the most straightforward way to strengthen your file.

Builder Qualification and Approval

This is where many applications hit unexpected delays. Lenders approve the builder alongside the borrower, and missing or incomplete contractor documentation is one of the most common reasons for holdups.

What lenders require from your contractor:

- Valid California contractor’s license (verified through the CSLB)

- General liability and workers’ compensation insurance

- Portfolio of completed projects with references

- Signed contract with a detailed scope of work and payment schedule

Working with a licensed, established contractor like Golden Gate Group makes this part of the process significantly smoother. When your builder already has clean licensing and a verified track record, underwriters can clear this stage quickly instead of spending time chasing paperwork.

California-Specific Considerations for Custom Home Builders

Building in California, especially in Silicon Valley, adds regulatory layers that directly affect your budget, timeline, and loan approval. These are the factors most out-of-state guides overlook.

Seismic Requirements

Bay Area projects must meet strict seismic design standards that affect foundation systems and structural framing. This adds to your total construction cost, which increases your loan amount. More importantly, if your plans do not meet current seismic code, the appraisal can come in lower than expected and limit how much you can borrow.

Permit Timelines in Bay Area Cities

Permit delays are one of the biggest hidden risks in Silicon Valley builds. They push back your start date and increase loan carrying costs.

| City | Typical Permit Timeline |

| Cupertino | 4 to 8 months |

| Palo Alto | 6 to 12 months |

| San Jose | 3 to 6 months |

In some Silicon Valley cities, the permitting process alone can push your start date back six months to a year.

ADU Regulations in California (2025)

Most single-family lots in California now allow at least one ADU and one junior ADU. These can be financed through renovation loans based on post-construction value, and in Bay Area markets a well-designed ADU can significantly improve your overall project economics.

Title 24 Energy Requirements

New builds must meet California’s energy efficiency standards covering insulation, HVAC, and solar. These add to upfront costs but tend to support stronger appraisals, which can work in your favor during underwriting.

CalHFA Programs

For eligible owner-occupant borrowers, CalHFA offers assistance programs that can be layered with construction financing to reduce upfront costs. Availability changes regularly, so confirm current options directly with a construction loan specialist.

How Your Choice of Builder Affects Your Loan Approval

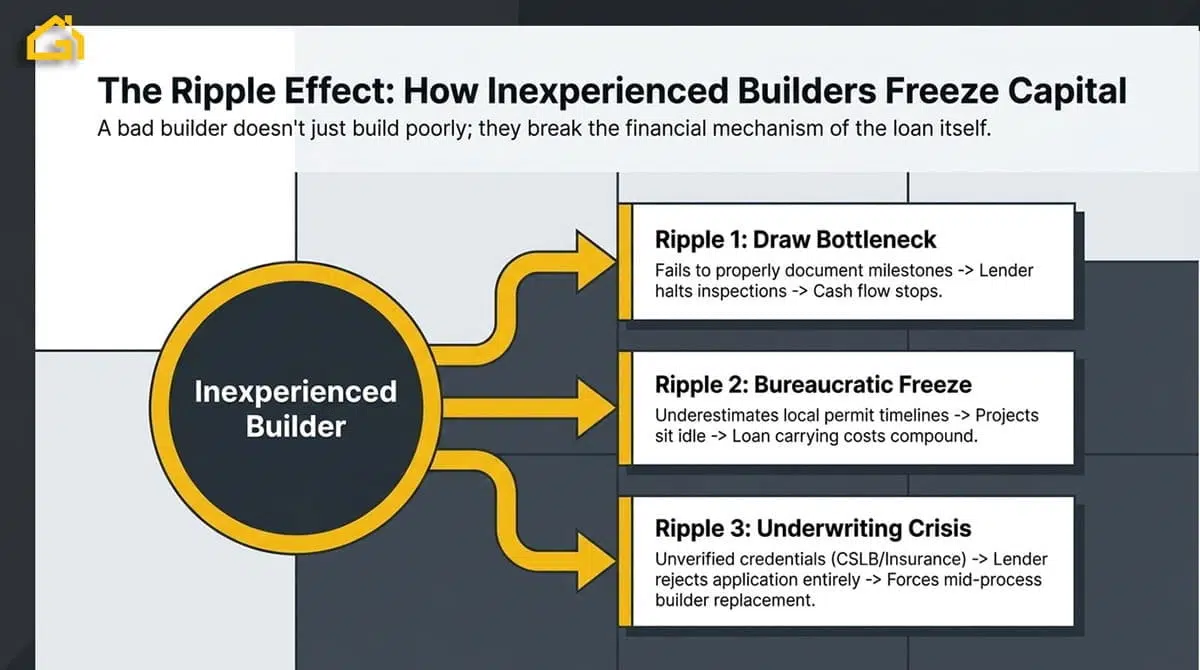

Most borrowers focus on their own financials when preparing for a construction loan, but lenders evaluate the contractor just as carefully. A builder with missing documentation or no verifiable track record can delay or derail an otherwise strong application.

What Lenders Look for in a Builder

Lenders are funding a project that does not exist yet, so the contractor’s history is their main evidence it will be completed on time and on budget. Before approving the loan, they will verify:

- Valid California contractor’s license (CSLB)

- General liability and workers’ compensation insurance

- Portfolio of completed projects with references

- Signed contract with detailed scope and cost breakdown

How Builder Experience Affects the Draw Process

Approval does not end at closing. Every fund release requires a lender inspection, and contractors who document milestones properly and schedule inspections without delays keep the project moving. Inexperienced builders often create bottlenecks here that compound over the course of a build and increase your carrying costs.

Why Local Experience in the Bay Area Matters

Contractors unfamiliar with Silicon Valley regularly underestimate permit timelines, seismic requirements, and local subcontractor availability. These miscalculations lead to budget overruns that put loans in jeopardy. A builder with a proven track record in Cupertino, Palo Alto, or San Jose knows how to price and plan accurately from day one, which reduces risk for both you and your lender.

Common Mistakes to Avoid When Getting a Construction Loan

Construction loans have more moving parts than a standard mortgage, and small missteps can create expensive problems down the line. These are the mistakes that come up most often.

- Underestimating the total budget: Bay Area construction costs are among the highest in the country. If your estimates are too conservative going in, you can find yourself short of funds before the project is complete, with limited options for additional financing mid-build.

- Choosing a builder without lender approval: Not every licensed contractor automatically qualifies. Signing a contract before confirming your builder meets the lender’s requirements can force you to restart the contractor selection process after you are already deep into the loan application.

- No contingency fund: Set aside 10% to 15% of the total project cost before you start. Unexpected site conditions, material price changes, and minor scope adjustments are normal parts of any build. Without a buffer, those costs come directly out of your pocket.

- Changing plans after closing: Design changes after loan approval require lender sign-off and sometimes trigger a new appraisal. What seems like a minor update can add weeks to your timeline and increase your overall costs.

- Ignoring soft costs: Permits, surveys, soil reports, architectural fees, and inspection costs are frequently left out of early budgets. In cities like Palo Alto and Cupertino, permit fees alone can run into the tens of thousands. These are real line items that need to be in your numbers from the start.

Permit fees, soil reports, and architectural drawings are often left out of early budgets, and in Bay Area cities, these numbers add up faster than most people expect, well before a single wall goes up.

Conclusion

Construction loans in California involve more moving parts than a standard mortgage, and in Bay Area markets the stakes are higher. Understanding the requirements, budgeting for the real costs, and partnering with a licensed local builder significantly increases your chances of a smooth approval and a successful build. Get these fundamentals right from the start and the rest of the process becomes much more manageable.